How to retire to Spain – and stop the taxman raiding your wealth

advertisement

Numerous people consider sunny Spain to be their ideal retirement location because of its gorgeous coastlines, mouthwatering cuisine, and vibrant culture. It should come as no surprise that more than 100,000 retired Britons have already relocated there.

Although moving to a warmer environment may be alluring, it is important to make preparations before making the move. Rushing it could result in unexpected tax payments and pension issues.

Everything you need to know about moving to Spain is covered here by Telegraph Money, including information on taxes, visas, pensions, and housing costs.

How much money will you need to retire in Spain?

Unlike persons of working age, pensioners are classified as "economically inactive" in Spain, which means they must meet additional conditions to remain in the nation.

The "non-lucrative visa" and the "golden visa" are the two categories of visas required to obtain the right to reside in the nation.

The non-lucrative visa demands evidence of your financial stability to pass an annual income check. The visa then has a two-year renewable period.

The required income is €28,800 (£25,043) as of 2023, plus €7,200 for each dependent for each year you reside in Spain. In addition, the immigration office will receive any savings.

When applying for a visa renewal, you must demonstrate that your income will persist for the entire duration or that you have about twice as much savings as when you first applied for the visa. Plan for an annual increase of roughly this size, as the income threshold increased by 3.5 percent last year.

THE STATE PENSION WILL SURPASS £10,000 FOR THE FIRST TIME THIS YEAR THANKS TO THE TRIPLE LOCK

To supplement your current £10,600 annual new state pension, you would need an additional €16,610 for a single person and €11,620 for a couple from other sources.

The "Golden Visa," which grants permanent legal residency without the need to reside in Spain for any period, maybe a more flexible option. However, it requires a €500,000 investment in real estate, €1 million in investment funds, bank deposits, or listed company shares in Spanish financial institutions, €2 million in Spanish government debt, or a €1 million investment in a business that creates jobs.

How you will be taxed in Spain?

Before relocating, anyone planning a relocation must take into account their financial and tax circumstances to avoid being hit with expensive bills.

The tax-efficient treatment of British investments, such as Isas and National Savings & Investments, is not the same abroad. Any interest, dividends, or capital gains generated by these accounts will be subject to taxation in Spain.

Pension income is subject to local income taxes where the pension bearer resides. Government employee pensions are the lone exemption, and they will only be taxed in the UK.

Importantly, if you take this after moving to Spain, the 25 percent tax-free pension cash rule will not be applicable. Because Spain does not have a non-taxable portion of a pension fund, your cash lump amount is taxable. Those that are proactive may be better off accepting the tax-free money before moving.

After moving, anyone who intends to sell their family property in Britain could be hit with fees.

"Most nations have some type of main house tax exemption, so under normal circumstances, there is no capital gains tax due on sales," explained Jason Porter of Blevins Franks. "However, the UK's rules are very different from those in Spain.

If the sale happens after you've left, it can result in tax liabilities in Spain, even if it might not in the UK.

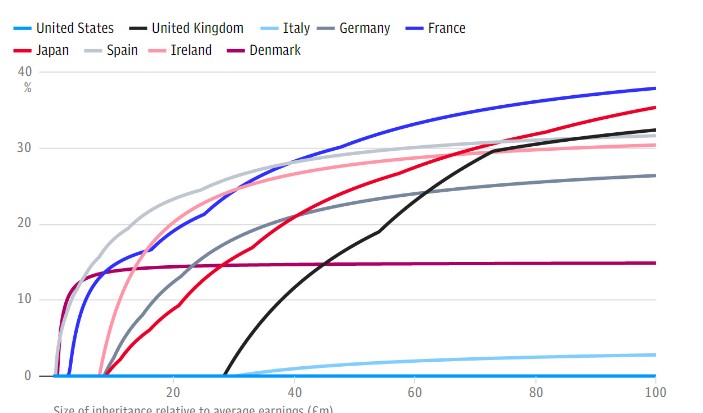

HOW COUNTRIES COMPARE ON INHERITANCE TAX

The sale of a British company delayed until after departure to avoid UK capital gains tax is also likely to be subject to tax in Spain, he continued.

Like other nations in Europe, Spain levies additional taxes on its citizens that the United Kingdom does not, such as a wealth tax. This calls for the completion of supplementary tax return forms by foreigners. Any assets worth more than €2 million must be disclosed on a wealth tax return.

More recently, other regions in Spain have debated replicating Madrid's 100 percent wealth tax exemption. Fearing a major drop in tax revenue, the national government opted to implement a new "solidarity tax" this year.

starting at 1.7 percent on wealth exceeding €3 million, up to 2.1 percent at €5 million, and 3.5 percent at €10 million.

Where both wealth tax and solidarity tax may be due, the same assets will not be taxed more than once by the taxpayer. A "Modelo 720" form must also be used to disclose overseas assets worth more than €50,000. If you don't, there could be serious consequences.

In Spain, there are significant regional differences in inheritance taxes. While other districts can impose death penalties of up to 34 percent, some locations, like Madrid, have a 100 percent exemption from inheritance tax.

Buying Spanish property

Property in Spain is significantly less expensive than a typical British home. According to estate company Knight Frank, the national average price per square meter in Spain is €1,625 (£1,396), as opposed to £2,863 in the United Kingdom. The lowest property value in the first three months of 2021 was in the Murcia region of southeast Spain, at €981 per square meter.

One of the requirements for the "golden visa" is having property worth more than €500,000 in Spain.

However, there are taxes, fees, and stamp duties associated with purchasing real estate in Spain. The consultant calculated that these expenses make up 11 percent of the price of the property being purchased. Conveyancing costs are an additional expense that typically accounts for 1% of the cost of the property.

Getting health coverage or insurance

Britons are required to have full health insurance and must demonstrate that they won't place an "undue burden" on the Spanish state.

A private health insurance plan with at least €30,000 in full coverage for the entire residency permit period is required for anyone seeking a visa.

(Writer:Tommy)

Related Articles